collective investment trust is one of the most important topics for US investors in 2026. If you’ve ever looked at your 401(k) statement and seen unfamiliar investment options with lower fees than mutual funds, you’ve likely encountered a collective investment trust. These pooled investment vehicles are growing rapidly in workplace retirement plans, yet most investors don’t understand how they work or why they might be paying less in fees compared to traditional mutual funds.

The collective investment trust market has grown to over $5 trillion in assets as of 2026, with more than 60% of 401(k) plans now offering at least one CIT option. Despite this explosive growth, surveys show that fewer than 25% of retirement savers can accurately explain what a collective investment trust is or how it differs from a mutual fund. This knowledge gap matters because the investment vehicle you choose can significantly impact your retirement savings over decades of compound growth.

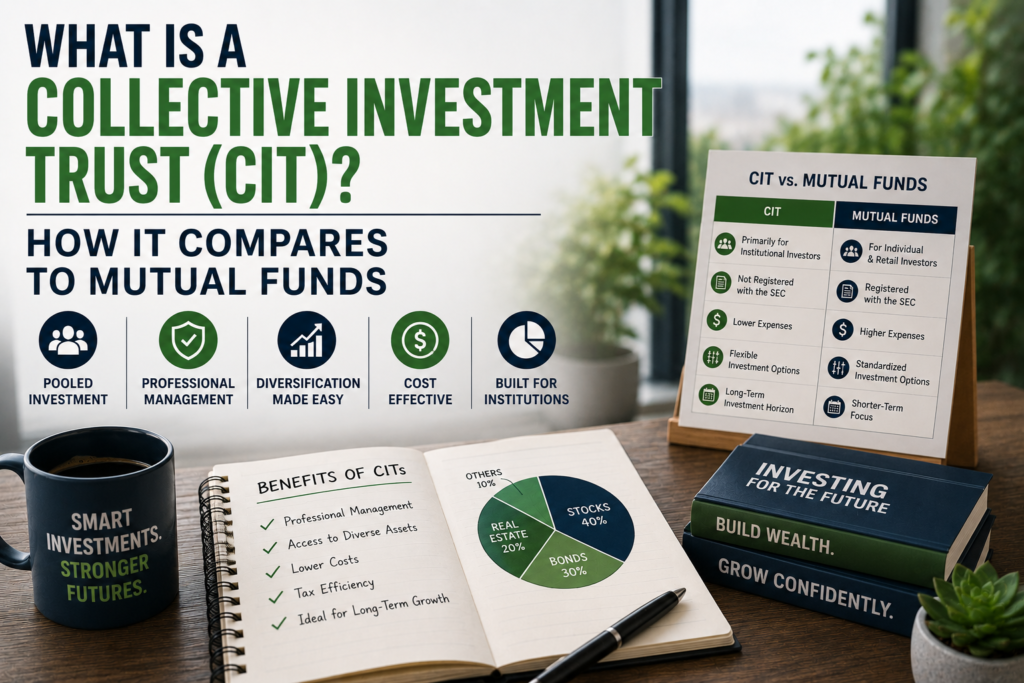

What Is collective investment trust?

A collective investment trust is a tax-exempt pooled investment fund maintained by a bank or trust company that is exclusively available to qualified retirement plans like 401(k)s, 403(b)s, and pension plans. Unlike mutual funds which are regulated by the Securities and Exchange Commission under the Investment Company Act of 1940, a collective investment trust is regulated by the Office of the Comptroller of the Currency under banking laws. This fundamental regulatory difference allows CITs to operate with lower overhead costs and pass those savings on to retirement savers through reduced expense ratios.

For example, imagine your employer offers both a large-cap stock mutual fund with a 0.50% expense ratio and a similar large-cap collective investment trust with a 0.15% expense ratio in your 401(k) plan. Both invest in nearly identical portfolios of large US companies, but the CIT costs 0.35% less annually. On a $100,000 investment over 30 years with 7% annual returns, that fee difference could result in over $75,000 more in your retirement account. This is why understanding collective investment trusts has become essential for maximizing your retirement savings.

Why collective investment trust Matters for US Investors in 2026

The shift toward collective investment trusts in retirement plans has accelerated dramatically, with industry data showing that CIT assets have grown by over 180% in the past decade while mutual fund assets in 401(k) plans have remained relatively flat. The average expense ratio for a collective investment trust is 0.25%, compared to 0.52% for the average mutual fund in retirement plans, representing a cost savings of more than 50%. For the 100 million Americans with 401(k) accounts, this fee differential translates to billions of dollars in potential savings annually.

- Lower Expense Ratios: Collective investment trusts typically charge 0.10% to 0.40% less in annual fees compared to equivalent mutual funds, allowing more of your investment returns to compound over time. This cost advantage exists because CITs don’t pay for SEC registration, don’t produce expensive shareholder reports, and don’t incur 12b-1 marketing fees.

- Institutional Pricing for Everyone: When you invest in a collective investment trust through your 401(k), you access the same institutional pricing that billion-dollar pension funds receive. This democratization of investment costs has leveled the playing field between small retirement savers and large institutional investors.

- Professional Management: Every collective investment trust is managed by experienced institutional investment managers at banks and trust companies with fiduciary obligations to plan participants. These same firms often manage billions in pension assets and bring that expertise to your workplace retirement plan.

- Tax Efficiency: Because collective investment trusts are structured as trusts rather than investment companies, they avoid certain operational complexities and costs associated with mutual funds. The tax-exempt status of CITs within qualified retirement plans also eliminates concerns about taxable distributions that can affect mutual funds in taxable accounts.

How to Get Started with collective investment trust: Step-by-Step

Accessing a collective investment trust is straightforward if your employer’s retirement plan offers them as investment options.

- Step 1: Review your 401(k) or 403(b) investment menu to identify which options are collective investment trusts. Log into your retirement account portal and look for investments labeled as “CIT,” “collective trust,” or “collective fund,” or check the fund prospectus or fact sheet which will indicate the legal structure. Some plan providers also list CITs with notations like “Class C” or “Trust” in the fund name.

- Step 2: Compare the expense ratios and investment strategies of available collective investment trusts to similar mutual funds in your plan. Use your plan’s comparison tools or request a fee disclosure document that shows all-in costs including expense ratios, administrative fees, and any revenue sharing arrangements. Pay attention to the investment objective, asset allocation, and historical performance to ensure you’re comparing truly similar investment options.

- Step 3: Reallocate your existing contributions and account balance to include collective investment trusts that match your risk tolerance and time horizon. Most plans allow you to make changes online instantly, with trades executing at the close of the business day. Consider maintaining a diversified portfolio across multiple asset classes regardless of whether you choose CITs or mutual funds.

- Step 4: Monitor your collective investment trust holdings quarterly and rebalance annually to maintain your target asset allocation. While CITs typically have lower costs, you should still review performance relative to appropriate benchmarks and ensure the investment strategy remains aligned with your retirement goals. Remember that you cannot transfer or roll over a CIT to an IRA while employed, so understand your plan’s rules about investment portability.

collective investment trust: Common Mistakes to Avoid

Many beginners make costly errors when evaluating a collective investment trust in their retirement plan, often because these vehicles are less familiar than mutual funds.

- Mistake 1: Assuming all CITs are automatically better than mutual funds. While collective investment trusts typically have lower fees, you must still evaluate the total cost including any plan-level administrative fees that might offset the expense ratio advantage. Some plans layer additional recordkeeping charges onto CITs that can narrow or eliminate the fee benefit, so always check the total cost of ownership.

- Mistake 2: Ignoring investment quality in favor of low fees alone. A collective investment trust with a 0.10% expense ratio is not a good deal if it’s poorly managed, doesn’t match your investment needs, or has tracking error that causes it to underperform its benchmark by more than the fee savings. Always evaluate the investment manager’s track record, the fund’s investment process, and whether the asset class fits your overall portfolio strategy.

- Mistake 3: Not understanding the liquidity restrictions of collective investment trusts. Unlike mutual funds which can be held in IRAs and taxable accounts, a collective investment trust can only be owned within a qualified retirement plan, which means you’ll need to sell and move to different investments if you leave your employer or retire. Some CITs also have redemption notice periods of 30-90 days, though most 401(k) plans negotiate daily liquidity for their participants.

Before making any investment decisions about collective investment trusts in your retirement plan, consider consulting with a financial advisor who can help you understand how these vehicles fit into your complete financial picture. The fee savings can be substantial, but they should be weighed against factors like investment quality, portfolio fit, and your specific retirement timeline.

For more information, visit Investopedia or the official SEC website.

Frequently Asked Questions About collective investment trust

What is collective investment trust and how does it work?

A collective investment trust is a pooled investment vehicle operated by a bank or trust company that combines assets from multiple qualified retirement plans to achieve economies of scale and lower costs. The trust is divided into units similar to mutual fund shares, and your 401(k) plan purchases units on behalf of participants who select that investment option. Because the collective investment trust is regulated under banking law rather than securities law, it has lower operational costs that translate to reduced expense ratios for investors.

Is collective investment trust a good option for beginners?

Yes, a collective investment trust can be an excellent option for beginner investors because the lower fees mean more of your money stays invested and compounds over time. CITs offer the same professional management and diversification as mutual funds but at a reduced cost, which is particularly valuable for long-term retirement savers. The main consideration is ensuring your 401(k) plan offers quality CIT options that align with your investment goals and risk tolerance.

How much money do I need to start with collective investment trust?

You don’t need any minimum investment amount to access a collective investment trust in your 401(k) plan beyond whatever minimum contribution your employer requires for plan participation. The collective investment trust structure allows even small investors to pool their money with others and access institutional pricing that would typically require millions of dollars to obtain directly. This makes CITs particularly valuable for younger workers or those just starting their retirement savings journey.

What are the risks of collective investment trust?

The investment risks of a collective investment trust are essentially the same as those of a comparable mutual fund—market risk, interest rate risk, credit risk, and other factors depending on the asset class. The main unique consideration is liquidity and portability, as you cannot directly own a CIT outside a qualified retirement plan and may face restrictions when leaving your employer. Additionally, CITs provide less public disclosure than mutual funds, so you may have access to fewer performance details and holdings information, though your plan fiduciary reviews this information on your behalf.

Conclusion: Is collective investment trust Right for You?

A collective investment trust represents one of the most significant fee-saving opportunities available to retirement savers in 2026, with cost advantages that can add tens or even hundreds of thousands of dollars to your nest egg over a career. If your 401(k) plan offers quality collective investment trust options that match your investment needs, choosing them over higher-cost mutual funds is often a smart decision that requires no additional effort or expertise. The key is to evaluate each CIT on its merits—considering fees, investment quality, and portfolio fit—rather than assuming all collective investment trusts are automatically superior to all mutual funds.

If you are ready to take the next step with collective investment trust, start your investment journey today and build the financial future you deserve.